Strategies to Supplement Your Clients’ Pension Income

Let’s talk pension retirement planning – it’s a big deal for many folks as they approach retirement. But with pensions changing and uncertainties popping up, it’s crucial to have solid strategies in place to top up that pension income.

So, grab a coffee, and let’s dive into some practical tips and insights to help you and your clients navigate this important aspect of retirement planning.

In this article, we’ll delve into key strategies to enhance pension retirement planning, offering detailed insights and actionable tips to help Financial Advisors navigate this critical aspect of their clients’ financial futures.

Understanding the Pension Retirement Planning Landscape

First things first, let’s understand what we’re working with.

Pensions come in all shapes and sizes, from the traditional defined benefit plans that promise a set monthly payout, to the 401(k) plans where employees stash away a portion of their paycheck each month. Each plan has its quirks and perks, so it’s essential to know the ins and outs of your clients’ pension setups.

Defined benefit plans promise a predetermined monthly benefit upon retirement, typically based on factors such as salary and years of service.

On the other hand, defined contribution plans, such as 401(k) or 403(b) plans, allow employees to contribute a portion of their salary to individual accounts, often with employer matching contributions.

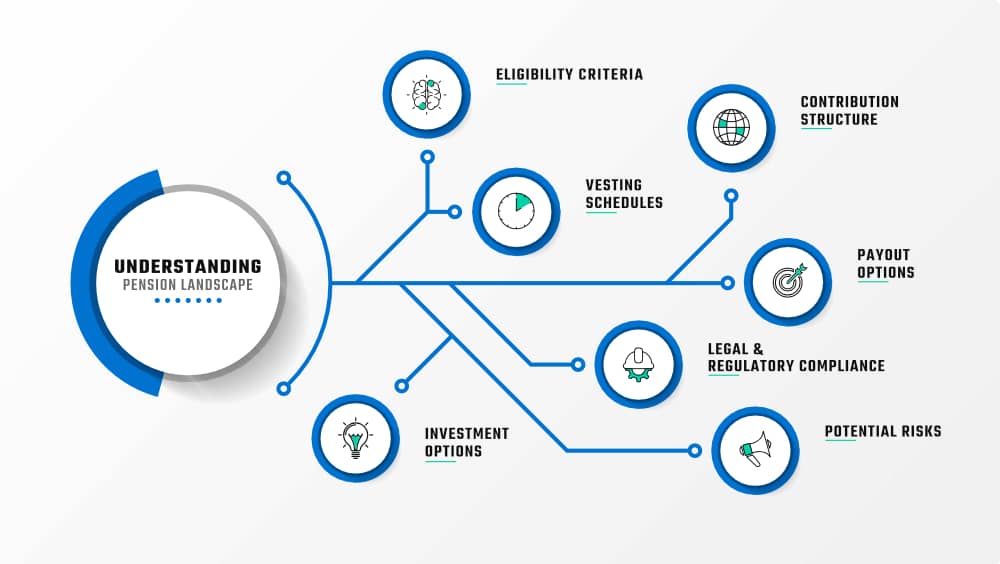

Financial Advisors must thoroughly understand the specifics of each client’s pension retirement planning, including:

Eligibility Criteria

- Determine who is eligible to participate in the pension plan. This may include full-time employees, part-time employees, or specific job classifications.

- Check if there are any eligibility requirements such as minimum age or length of service.

Vesting Schedules

- Understand the vesting schedule, which determines when employees become entitled to the employer’s contributions to their pension accounts.

- Determine if the vesting schedule is graded (incremental vesting over time) or cliff-vesting (100% vesting after a certain period).

Contribution Structure

- Examine how contributions are made to the pension plan, whether they are made solely by the employer, employee, or a combination of both.

- Determine if there are any matching contributions provided by the employer and the vesting schedule associated with them.

Payout Options

- Explore the various payout options available to participants upon retirement. This may include lump-sum distributions, annuity payments, or a combination of both.

- Understand the implications of each payout option on taxes, retirement income sustainability, and estate planning.

Investment Options

- Review the investment options offered within the pension plan. This may include a range of investment funds such as stocks, bonds, mutual funds, or target-date funds.

- Assess the performance history, fees, and risk profile of each investment option to ensure they align with clients’ retirement goals and risk tolerance.

Potential Risks

- Identify potential risks associated with the pension plan, such as underfunding, investment risk, longevity risk, or changes in plan design.

- Evaluate the financial stability of the plan sponsor (employer) and the Pension Benefit Guaranty Corporation (PBGC) insurance coverage for defined benefit plans.

Legal and Regulatory Compliance

- Ensure that the pension plan complies with relevant laws and regulations, including the Employee Retirement Income Security Act (ERISA), Internal Revenue Code (IRC), and Department of Labor (DOL) requirements.

- Stay informed about any changes in legislation or regulatory guidance that may affect the pension plan and its participants.

By thoroughly understanding these aspects of each client’s pension retirement planning you can provide informed guidance, tailor supplemental strategies, and help your clients make confident decisions about their retirement futures.

Maximizing Retirement Savings Vehicles

Now, onto the good stuff – maximizing retirement savings!

While employer-sponsored retirement accounts like 401(k)s or 403(b)s offer fantastic tax advantages and are a cornerstone of pension retirement planning, let’s not overlook another powerful tool in your arsenal: individual retirement accounts (IRAs).

IRAs come in different flavors, but one that deserves special attention is the Roth IRA. Unlike traditional IRAs, contributions to a Roth IRA are made with after-tax dollars, meaning withdrawals in retirement are tax-free. This can be a game-changer for clients looking to diversify their tax strategies in retirement.

Advantages of Roth IRAs

Tax-Free Withdrawals

As touched upon above, unlike traditional IRAs where contributions are tax-deductible but withdrawals are taxed, Roth IRA contributions are made with after-tax dollars, allowing for tax-free withdrawals in retirement.

This can be incredibly beneficial for clients in higher tax brackets or those expecting to be in a higher tax bracket in retirement.

Flexible Withdrawal Rules

Roth IRAs offer more flexibility in withdrawal rules compared to traditional IRAs. Contributions (not earnings) can be withdrawn penalty-free at any time, making Roth IRAs a useful source of emergency funds or for other short-term financial needs.

No Required Minimum Distributions (RMDs)

Roth IRAs do not have required minimum distributions (RMDs) during the account owner’s lifetime, unlike traditional IRAs and employer-sponsored retirement accounts. This allows for greater control over retirement income and potential tax planning opportunities.

Estate Planning Benefits

Roth IRAs can be powerful estate planning tools, as assets can be passed on to heirs tax-free. This can provide a significant legacy for future generations and may offer estate tax advantages.

Important Considerations with Roth IRAs

Eligibility and Contribution Limits

Roth IRAs have income limits for eligibility and contribution amounts. For 2024, the ability to contribute to a Roth IRA begins to phase out at certain income levels and is completely phased out above specific thresholds.

It’s essential to understand these limits and plan contributions accordingly.

Conversion Strategies

For clients who exceed the income limits for direct Roth IRA contributions, consider implementing a backdoor Roth IRA strategy. This involves making nondeductible contributions to a traditional IRA and then converting them to a Roth IRA. However, be mindful of the pro-rata rule and potential tax implications.

Investment Options

Roth IRAs offer a wide range of investment options, including stocks, bonds, mutual funds, ETFs, and more. Work with your clients to develop a diversified investment strategy that aligns with their risk tolerance and long-term financial goals.

Long-Term Growth Potential

Roth IRAs can provide significant long-term growth potential, especially for younger clients who have many years until retirement. With tax-free growth potential, Roth IRAs can be powerful wealth-building tools over time.

Common Misconceptions about Roth IRAs

Roth IRAs are only for young people

Reality: While starting early with Roth IRA contributions can maximize growth potential, Roth IRAs can be valuable for individuals of all ages, especially those seeking tax diversification in retirement.

Roth IRAs are subject to contribution limits similar to traditional IRAs.

Reality: Roth IRAs have the same contribution limits as traditional IRAs, but eligibility for contributions may be limited based on income levels.

Roth IRAs are only beneficial for individuals in lower tax brackets

Reality: Roth IRAs can provide significant tax advantages for individuals in higher tax brackets, especially if they anticipate being in a similar or higher tax bracket in retirement.

By maxing out contributions to both employer-sponsored plans and IRAs, clients can take full advantage of tax-deferred growth opportunities, ensuring they have a robust nest egg when retirement rolls around.

So, don’t sleep on IRAs – they’re an essential piece of the retirement savings puzzle!

Diversifying Investment Portfolios

Time to get a bit creative with investments!

Diversification is a fundamental principle of investment success, particularly when supplementing pension income. Financial Advisors should work with clients to develop diversified investment portfolios that align with their risk tolerance, time horizon, and retirement objectives.

A well-diversified portfolio may include a mix of equities, bonds, real estate investment trusts (REITs), and other asset classes to spread risk and enhance return potential.

Additionally, Advisors should explore alternative investments, such as private equity, hedge funds, and commodities, to further diversify portfolios and potentially enhance returns.

Alternative investments offer low correlation to traditional asset classes, providing potential downside protection during market downturns and enhancing portfolio resilience.

Implementing Annuities for Guaranteed Income

Let’s talk annuities – they’re like the Swiss Army knife of retirement planning!

Advantages of Annuities

Annuities can provide a guaranteed income stream to supplement pension retirement planning benefits, offering a safety net in uncertain times. Plus, they come with tax benefits and can help ease worries about outliving your savings. It’s all about that peace of mind, right?

Income Certainty

Annuities provide a guaranteed income stream, offering peace of mind and financial security in retirement.

Immediate annuities provide immediate income payments, while deferred annuities allow for income payments to start at a later date, providing flexibility to meet individual retirement needs.

Principal Protection

Annuities offer protection against market volatility and investment risk.

With immediate annuities, the premium is converted into guaranteed income payments, protecting the principal from market fluctuations.

Deferred annuities offer the opportunity for asset accumulation with downside protection features, safeguarding the invested capital.

Tax-Deferred Growth

Annuities offer tax-deferred growth, allowing investments to grow without being subject to annual taxation. This can enhance accumulation potential over time and may result in greater retirement income compared to taxable investments.

Longevity Risk Mitigation

Annuities help mitigate longevity risk, the risk of outliving one’s savings in retirement.

By providing guaranteed income for life or a specified period, annuities ensure a steady stream of income regardless of how long retirement lasts.

Important Considerations for Annuities

Understanding Product Features

Annuities come in various forms, including fixed, variable, indexed, and immediate annuities. Each type has unique features, benefits, and considerations.

It’s essential to understand the product features, such as payout options, withdrawal provisions, surrender charges, and fees, to determine the suitability for clients’ retirement needs.

Evaluating Financial Strength

When selecting annuity products, consider the financial strength and reputation of the insurance company issuing the annuity.

Look for companies with strong credit ratings and a history of financial stability to ensure the safety and security of clients’ investments.

Assessing Surrender Charges and Fees

Annuities may have surrender charges and fees associated with early withdrawals or surrendering the contract before the end of the surrender period. Understand the terms and conditions of the annuity contract, including any applicable charges or fees, and how they may impact clients’ overall retirement plans.

Common Misconceptions about Annuities

Annuities are too complex

Reality: While annuities may have intricate features, with proper education and guidance from Financial Advisors, clients can understand how annuities work and how they can benefit from incorporating them into their retirement portfolios.

Annuities are expensive

Reality: While some annuities may have fees, the benefits they offer, such as guaranteed income and principal protection, often outweigh the costs, especially when tailored to clients’ specific needs and objectives.

Annuities lack flexibility

Reality: With a diverse array of annuity products available, Financial Advisors can customize solutions that align with clients’ unique preferences, providing flexibility and adaptability throughout their retirement journey.

Empire Marketing Partners believes in the benefits of annuities, including income certainty, principal protection, and tax-deferred growth.

By incorporating annuities into retirement portfolios, you can help your clients mitigate longevity risk, ensure a steady stream of income throughout retirement, and provide peace of mind in uncertain market environments.

Long-Term Care Planning

Last but not least, let’s talk long-term care. It’s not the most fun topic, but it’s crucial to plan for those potential healthcare costs down the road.

Whether it’s long-term care insurance, hybrid life insurance policies, or good old-fashioned savings, having a plan in place can help protect retirement assets and keep those worries at bay.

Phew, we covered a lot, didn’t we?

But hey, that’s what pension retirement planning is all about – helping your clients take charge of their financial future and making sure they’re set for a comfortable retirement.

As a Financial Advisor you provide the knowledge and expertise to help your clients achieve greater financial security and peace of mind in pension retirement planning.

With proactive planning and strategic guidance, your clients can enjoy a fulfilling retirement that aligns with their goals and aspirations, supported by Empire Marketing Partners’ emphasis on the benefits of annuities in pension retirement planning.

So, keep these tips in your back pocket, and remember, Empire Marketing Partners is here to help you every step of the way. Together, let’s boost your client’s retirement incomes and make those golden years truly shine!